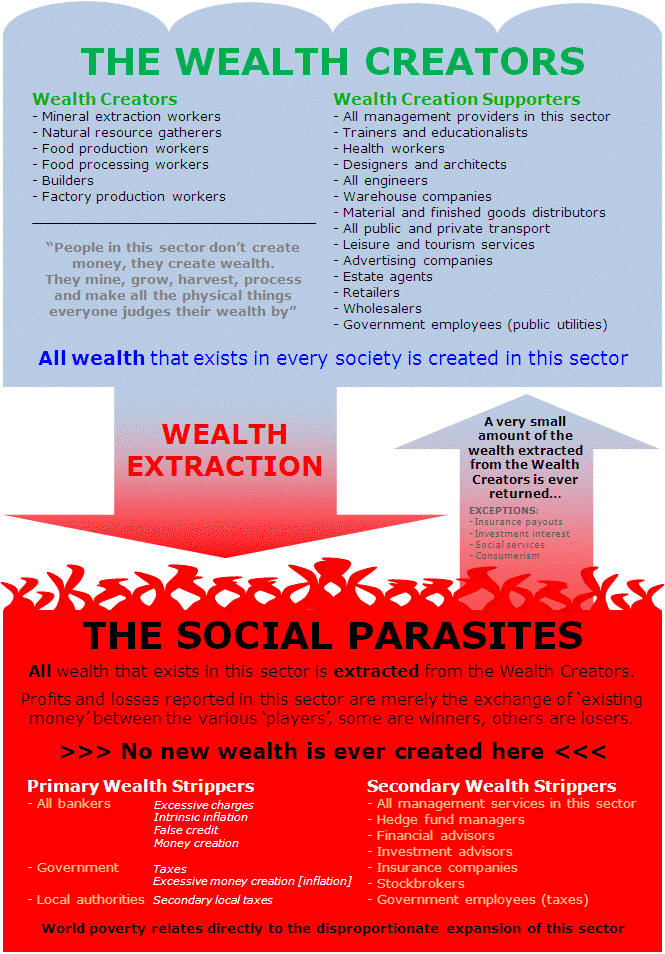

Research as much as you like, in fact the more you research the more financial instruments you will find. Hundreds in fact all with fancy names and equally fancy effects on the financial system.

But if you cut through all the mystique, all the complicated explanations, it all comes down to one thing, they are all ways to extract wealth from the wealth creators; nothing more.

Economists will have you believe that these mechanisms are there to ensure proper functioning of the financial system. If regular boom-bust, recession-depression cycles are the financial system functioning properly then I think most of us can do without it.

How The Banks Earn A Crust

The first step is to prize that first chunk of money from the unwary, stupid, blinkered, too busy creating wealth to see or care, public. Now, with this first chunk of un-earned money in their clammy palm the banks and financial institutions are in a position to start working their magic.

(Picture at this point a portly banker smiling, hands raised, elbows tucked in, gently rubbing his fingers with his thumbs).

All the money in the financial system starts from this humble beginning. You have to understand that most of the money in the financial services sector was originally either borrowed or plucked out of thin air. They make nothing, they create nothing [misery excepted], they create no real wealth, all their money is acquired initially from investors. Very approximately the ratio between real money and thin air money in the financial system is 1:10.

Before I go on, let’s just summarize the three broad types of investor.

- The private investor, a wealth creator or wealth creator supporter who has surplus wealth and wishes to place it in a money warehouse [bank] for ‘safe keeping’ [?]. However in order to counteract the effects of that other global fraud ‘inflation’ he requires payment of interest on the deposit so that his money retains its original value (purchasing power).

- The institutional investor is typically a pension fund or similar institution that has extracted some real wealth from a sector of the public on the promise of a future return. Institutional investors gamble on the financial markets to maximize profits for themselves while at the same time providing a modest return for their investors. Like all gambling operations there will be winners and losers. Just your hard luck if your pension fund is in the hands of one of the losers, that you have no say in the matter is another ‘unlegislated for’ social crime.

- Finally there are the financial institutions that use a combination of money made up from real money investments and the re-investment of money made from money that did not exist or was made from dealing (taking risks) with other people’s (or institutions ‘thin air’) money. The lowest of the low, these people are true social parasites. Success for them is risking other people’s money for their own gain, they make nothing, they contribute zero to society, they should be exposed and labeled as the social pariahs they are.

Of all trading on the financial services market, roughly 75% is made by financial institutions (groups 2 and 3), only 25% is made by small private investors.

I know I’ve mentioned before the use the banks make of the reserve ratio system to acquire money for themselves, but because this abhorrent practice has such a fundamental effect of the financial system, provides excessive wealth for the bankers and has such a negative effect on everyone else, I feel obligated from time to time to try and find ever more simple ways to explain the principles of such a repugnant and socially abhorrent system.

The Wikipedia entry for the ‘Reserve Requirements’ for banks includes a paragraph on its effect on the money supply. I know most people think that Governments have a monopoly on the money supply, but this is a misconception, even banknotes are printed by the central bank and they are privately owned (by the banks). So back to Wikipedia, which explains very succinctly just how this marvelous little [sic] scheme works for the banks.

Remember that small initial chunk of money the bank acquired from the innocent investor, let’s make the amount just $100, well, the world banking cartel (with the complete backing of Government) is now able to lend 90% of that $100 back to the public. Mr public now puts the borrowed $90 back into the bank, the bank is now able to lend 90% of the $90 ($81), and so on. To show the end result of this, what can only be called a Ponzi Scheme, a small mathematical equation is necessary, for which I apologize:

($100+$90+81+$72.90+… = $1,000), e.g.$100/0.10 = $1,000.

So, that small initial $100 deposit of real money into the bank makes their annual balance sheet look something like figure 1 at the bottom of this article:

I know it begs the question, ‘so why are we not all bankers’? Well because if we were all bankers the human race would soon be just billions of naked people wandering around in a global forest.

But let’s move on, it doesn’t end there, the bankers acquire so much money from this interest on money that doesn’t exist scheme they not only live very well indeed but they have vast amounts of surplus money with which to create other equally devious financial schemes (collectively called financial instruments which somehow makes them sound more acceptable) that double and triple up their illicit profits. Not to mention the control such power gives them over Governments, inflation and almost every other scourge the ordinary people of the world have to suffer.

That almost every western country condones this banking fraud says something for the cleverness of the banking sector. So established is the system that modern day economists discuss the pros and cons of the system on the basis of it being ‘normal’. The reserve ratio (10% in the example given above) varies from country to country and can be set at anything between 0% and ‘no limit’. The USA reserve ratio is currently 10% while in the UK there is no limit. ‘No limit’ means the banks can create ‘thin air money’ and issue credit with no upper limit. By careful control the banks in any country can fine tune the money supply to such a precise level that most of the time they are able to extract the maximum amount of wealth from the wealth creators without causing the system to collapse.

However, such a hybrid system cannot go on ad infinitum, every so often the banks do get it wrong and the piper has to be paid. The result is a sudden collapse of the financial system followed by inevitable recession leading occasionally to a full blown depression. Of course there are cynics that believe the banks actually engineer the boom-bust-recession cycle for their own ends.

That the banks are in a position to wreak such havoc and inflict such misery on the public is a modern day social crime. That they [the banks] are able to protect themselves from the full force of economic meltdowns by recruiting the help of Governments is unbelievable. I am sure that one day historians will look back on this period of economic history with amazement, dumbfounded that such an obvious crime against society persisted for so long.

So to put the situation in it’s simplest terms, most of the money the banks lend does not exist. How can that be? Money either exists or it doesn’t. Well in most cases the banks don’t actually issue banknotes they issue checks, promissory notes, credit or debit cards, which because all banks have agreed to participate in the fraud the amount of money actually swirling around in the system never really gets audited.

But of course the fraud is one thing, its pernicious effect on the economy and ultimately on society is quite another. That it causes inflation goes without saying. By making so much money available through uncontrolled credit, over and above the ‘money supply’, it’s basic economics that the price of all goods will rise as the system re-adjusts the balance between the ‘new’ value of money and the limited supply of goods available. This is intrinsic inflation, not to be confused with the everyday inflation created and maintained by government as a final consumer tax.

Just a couple of topical points to finish off (circa 2009)

- BlackRock have just acquired a division of Barclays Bank creating a firm with over $2.7 trillion under management.

($2.7 trillion, that’s two million seven hundred thousand MILLIONS and this is just one firm, where did all that money come from? For the answer to where most of it appeared from, refer to the text above:)

- Bail-out banks want to pay back TARP money…

(Excuse me, the world is currently in the grip of a bank induced recession, bordering on depression, where the’ are these banks getting the ‘pay-back’ money from?).

Of course it’s understandable that the banks want to repay the money now since the longer the government hangs on to the shares the more the taxpayers are likely to make in the future as the recession subsides and the banking sector shares rise. Now that would not suit the banks at all, ‘the public making money out of the banks?’ A state of affairs that is totally unacceptable.

Figure 1

How to create money out of thin air:

| Item |

Receipts |

Outgoing |

Lending |

| Initial amount deposited |

$100 |

– |

– |

| Interest paid to the investor |

– |

$5 |

– |

| Amount lent to the public |

– |

– |

$1000 |

| Interest received by bank |

$100 |

– |

– |

| Bank profit/annum/$100 |

$95 |

– |

– |

{kind=link}